Code

%load_ext autoreload

%autoreload 2The autoreload extension is already loaded. To reload it, use:

%reload_ext autoreloadHere is a link to the source code for this Linear Regreession blog post. ### Link to reference for this blog post Here is a link to the main reference we use as we implement our linear regression model.

In this blog post let us take a look at Linear Regression. Linear regression, especially OLS (ordinary least squares) regression, is the bread and butter of many fields like economics and statistics. When we first learn about OLS regression, often times it was in some other setting, at least for yours truly. I have learned this in a economics class on regression analysis. However, we could easily formulate the same concept in a way that’s closer to the style of machine learning, and specifically classification tasks. For OLS linear regression, the loss function is \[ \ell (\hat{y}, y) = (\hat{y} - y)^2, \] where \(\hat{y} = \langle w, x \rangle\) is the predicted labels (which the inner product of \(w\), the weights, and \(x\), our data point), and \(y\) is the true label. Hence, when we are trying to minimize loss, we are trying to minimize the squared difference between our prediction and the true label. The empirical risk minimization problem is \[ \hat{w} = \argmin_{w} L(w) \\ \] where \[ L(w) = \sum_{i=1}^n (\hat{y}_i - y_i)^2 = \lvert \lvert Xw - y \rvert \rvert ^2_2.\\ \] Hence, least square is simply referring to minimizing the sum of squares for the loss function.

Before we start the implementation, we first record the following code snippet that will help us to automatically load our source code when we are constantly editing the .ipynb and .py files.

%load_ext autoreload

%autoreload 2The autoreload extension is already loaded. To reload it, use:

%reload_ext autoreloadFirst, let’s import some libraries, then we perform our fit_gradient and fit_analytic on the following simple data set with only one features to visualize our linear regression.

import numpy as np

np.random.seed(42)

from matplotlib import pyplot as plt

import matplotlib

plt.rcParams["figure.figsize"] = (18,6)

plt.rcParams['figure.dpi'] = 156

plt.rcParams['savefig.dpi'] = 156

from linear_regression import LinearRegression from sklearn.linear_model import Lasso

L = Lasso(alpha = 0.001)fit_gradientIn fit_gradient, the key step is to compute the gradient using a descent algorithm so that we could solve the following problem: \[ \hat{w} = \arg \min_{w} L(w). \] Equivalently, we could unpact this equation: \[ \hat{w} = \sum_{i=1}^{n} \ell(\hat{y}_i, y_i) = \argmin_{w} \sum_{i=1}^{n} ( \langle w, x_i \rangle - y_i)^2.\] Recall that our loss function is of the form $ (, y) = (-y)^2 $ since we are using ordinary least square regression.

We start by taking derivative with respect to \(w.\) Using chain rule for matrices, we obtain the following expression: \[ \nabla L(w) = 2 X^{T}(X\cdot w -y).\] Then, we use gradient descent to find the \(w\) that is “good enough.” We achieve this by the following iteration: \[ w^{(t+1)} \leftarrow w^{(t)} - 2 \cdot \alpha \cdot X^{T} (X \cdot w^{(t)} - y).\]

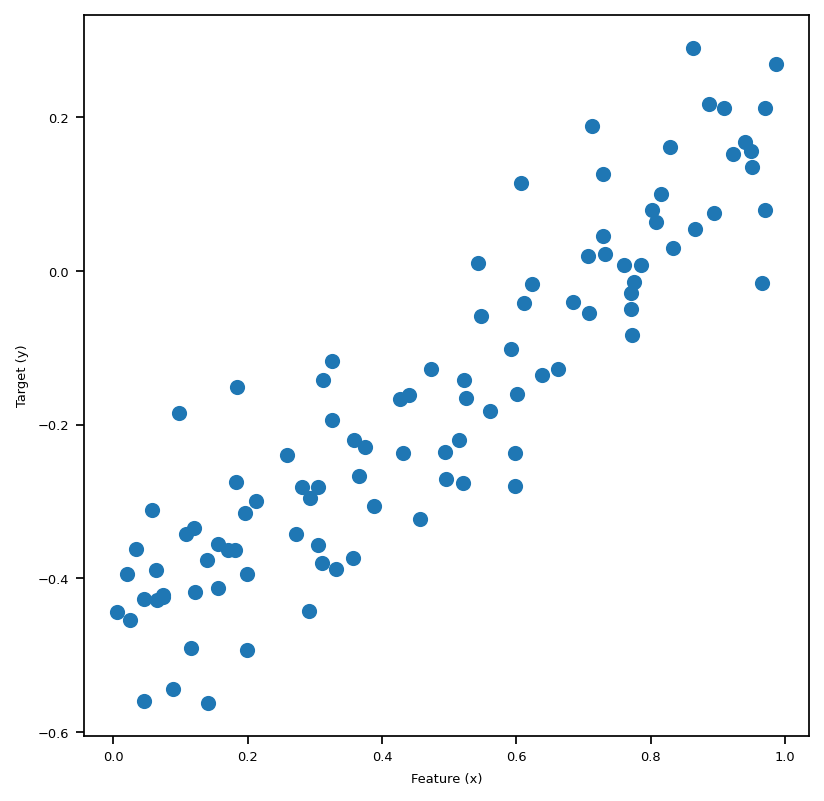

We use the following code block to generate a small data set for testing our linear regression implementation. Let’s plot our data, and in this 2-Dim case we could see the linear pattern with our eyes, and it’s quite intuitive that the best-fit-line obtained by our algorithm should also “fit” the data visually as if we were to draw it by hand on the plot of this sythetic data set.

# We start by generate a small data set.

w0 = -0.5

w1 = 0.7

n = 100

x = np.random.rand(n, 1)

y = w1*x + w0 + 0.1*np.random.randn(n, 1)

plt.figure(figsize=(6,6))

plt.scatter(x, y)

labels = plt.gca().set(xlabel = "Feature (x)", ylabel = "Target (y)")

We are able to generate data and visualize this problem when p_features = 1. Graphically, we are trying to draw a line “of best fit” through the data points in the sense of OLS, which stands for Ordinary Least Squares. The line we draw just means given the feature x, we find the corresponding predicted y using the line, which will be close to the original y, if we have done a good job.

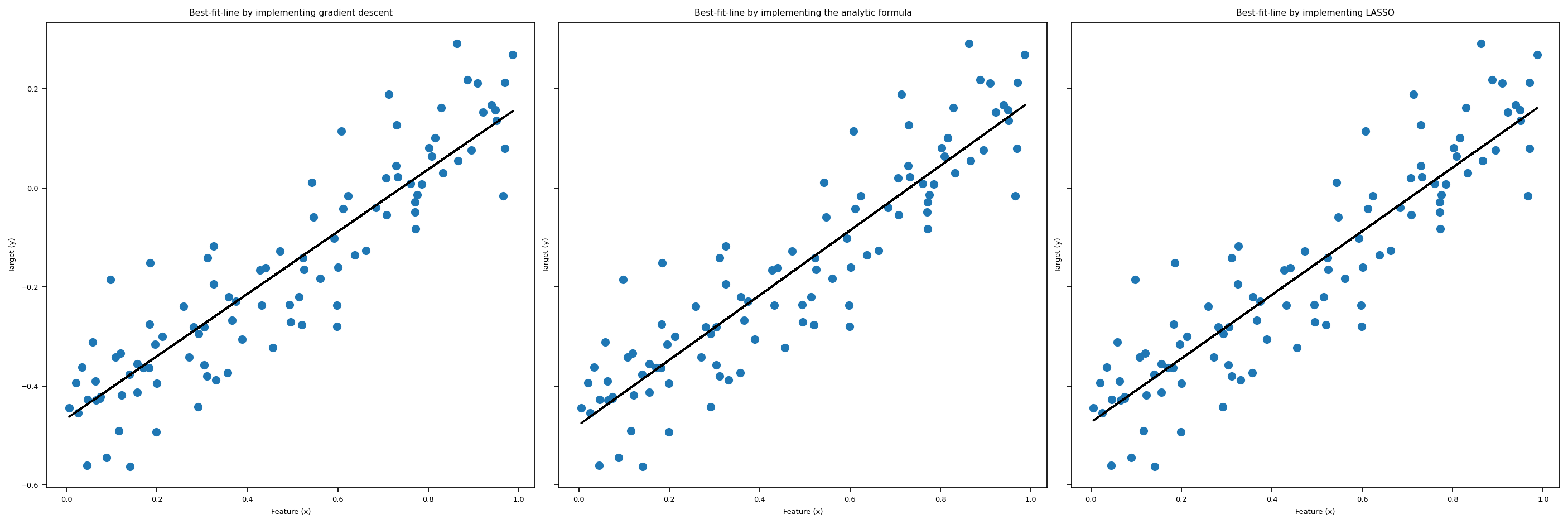

After importing linear_regression.py, we could call the fit_gradient method that implements the gradient descent algorithm for us, as illustrated in the above cell. In the following cell, we plot the “line of best fit” using the weights LR1.w that we obtained after running fit_gradient. Also, we print out the weights vector w that we fited, which seems to be doing a good job judging from the pictures below, plotted together with Lasso and fit_analytic.

LR1 = LinearRegression()

X_ = LR1.pad(x)

LR1.fit_gradient(X_, y, alpha=0.0001, max_epochs=1e4)

print(f"the weights that we obtained after calling fit_gradient are: {LR1.w}")the weights that we obtained after calling fit_gradient are: [[ 0.62864267]

[-0.46564827]]scikit-learnRoughly, LASSO algorithm is OLS regression plus a regulariation term, so the loss function looks like this: \[

L(w) = \lvert \lvert Xw - y \rvert \rvert ^2_2 + \lvert \lvert w' \rvert \rvert_1.\\

\] Where \[

\lvert \lvert w' \rvert \rvert_1 = \sum_{j=1}^{p-1} |w_j|.\\

\] Hence, we could think of this regularization term as some sort of penalty term when we have problems with overparameterization. In this post, we are not going to dive deep into the details of LASSO regression, so we are just going to use the implementation from scikit-learn. Again, we plot the result of fitting this regression together with the fit_gradient and fit_analytic in the big visualization below.

L.fit(x,y)

L.score(x,y)

print("*")

L_w = np.hstack([L.coef_, L.intercept_])

print(f"the weights that we obtained after calling fit_gradient are: {L_w}")*

the weights that we obtained after calling fit_gradient are: [ 0.6426091 -0.47312394]fit_analyticSimilarly to fit_gradient, we also have a method called fit_analytic, which uses a formula to compute the weights w exactly, and this is implemented using the followiing equation: \[ \hat{w} = (X^T X)^{-1} X^T y, \] where \(\hat{w}\) denotes the weights we obtained after calling the function fit_analytic. Note that in order for this formula to make sense, we need X to be a invertible matrix. Now, with the math part out of the way, let’s see this in action in the following block, where we plot the three regressions we introduced so far together in one plot.

matplotlib.rc('font', size=6)

# gradient

LR1 = LinearRegression()

X_ = LR1.pad(x)

LR1.fit_gradient(X_, y, alpha=0.0001, max_epochs=1e4)

fig, axarr = plt.subplots(1, 3, sharex = True, sharey = True)

axarr[0].scatter(x,y)

axarr[0].plot(x, X_@LR1.w, color = "black")

# Analytic

LR2 = LinearRegression()

X_ = LR2.pad(x)

LR2.fit_analytic(X_,y)

axarr[1].scatter(x,y)

axarr[1].plot(x, X_@LR2.w, color = "black")

# LASSO

axarr[2].scatter(x,y)

axarr[2].plot(x, X_@L_w, color = "black")

labs = axarr[0].set(title="Best-fit-line by implementing gradient descent", xlabel = "Feature (x)", ylabel = "Target (y)")

labs = axarr[1].set(title="Best-fit-line by implementing the analytic formula", xlabel = "Feature (x)", ylabel = "Target (y)")

labs = axarr[2].set(title="Best-fit-line by implementing LASSO", xlabel = "Feature (x)", ylabel = "Target (y)")

plt.tight_layout()

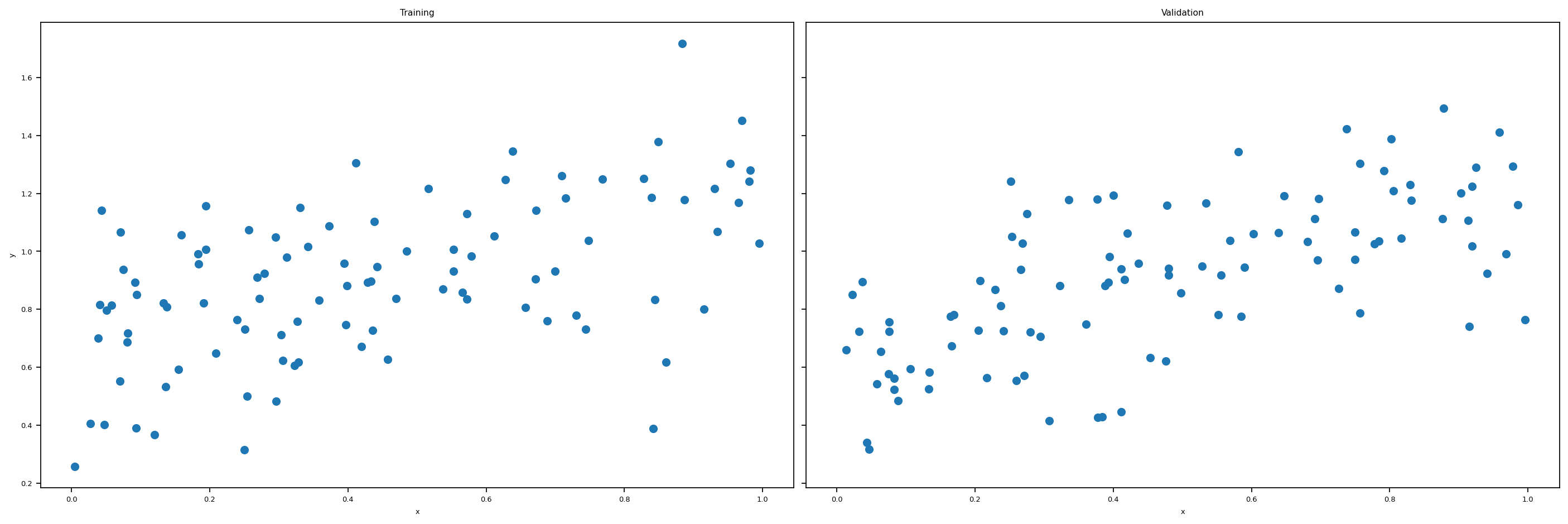

Now we use the following function to create both testing and validation data. At this stage, we could experiment with more features. We use the following code to create artificial data sets that has any number of features that we specify.

def LR_data(n_train = 100, n_val = 100, p_features = 1, noise = .1, w = None):

if w is None:

w = np.random.rand(p_features + 1) + .2

# print(w)

X_train = np.random.rand(n_train, p_features)

y_train = LR.pad(X_train)@w + noise*np.random.randn(n_train)

X_val = np.random.rand(n_val, p_features)

y_val = LR.pad(X_val)@w + noise*np.random.randn(n_val)

return X_train, y_train, X_val, y_valWhen the number of features is one, p_features = 1, we could plot the artificial training data set and the validation data set. We lose this luxury when we have 2 or more features. Let’s plot the data set we are going to use.

n_train = 100

n_val = 100

p_features = 1

noise = 0.2

# create some data

LR = LinearRegression()

X_train, y_train, X_val, y_val = LR_data(n_train, n_val, p_features, noise)

# plot it

fig, axarr = plt.subplots(1, 2, sharex = True, sharey = True)

axarr[0].scatter(X_train, y_train)

axarr[1].scatter(X_val, y_val)

labs = axarr[0].set(title = "Training", xlabel = "x", ylabel = "y")

labs = axarr[1].set(title = "Validation", xlabel = "x")

plt.tight_layout()

Now we experiment with the number of features being n_train - 1, which is quite a lot features. Are we going to have a high training score? Let’s find out!

n_train = 100

n_val = 100

p_features = n_train - 1

noise = 0.2

# create some data

X_train, y_train, X_val, y_val = LR_data(n_train, n_val, p_features, noise)Here’s the snippets within the fit_gradient function that makes the same code work for different number of features:

features = X_.shape[1]

self.w = np.random.rand(features)

from linear_regression import LinearRegression

LR = LinearRegression()

X_train_ = LR.pad(X_train)

X_val_ = LR.pad(X_val)

LR.fit_analytic(X_train_, y_train) # I used the analytical formula as my default fit method

print(f"Training score = {LR.score(X_train_, y_train).round(4)}")

print(f"Validation score = {LR.score(X_val_, y_val).round(4)}")Training score = 0.0333

Validation score = -0.2332We see that our training score is very close to zero, hence very low.

print(f"The estimated weight vector w is: {LR.w}")

print(f"Training Loss = {LR.Big_L(X_train_, y_train).round(2)}")

print(f"Validation Loss = {LR.Big_L(X_val_, y_val).round(2)}")The estimated weight vector w is: [-1.60048517 -3.1978511 0.80566383 1.10203529 1.36187644 -0.47123621

1.06288478 -0.49759679 0.88232925 -3.21484205 1.00067548 -0.85983013

0.36202332 0.61615846 3.23278271 0.49621812 1.51714629 -1.97442441

2.91490824 -0.56270441 1.34873889 -4.33324786 -3.39289948 -1.86798015

-4.24483306 -3.9345999 -0.38623783 0.77311176 2.2738731 15.68998649]

Training Loss = 0.0

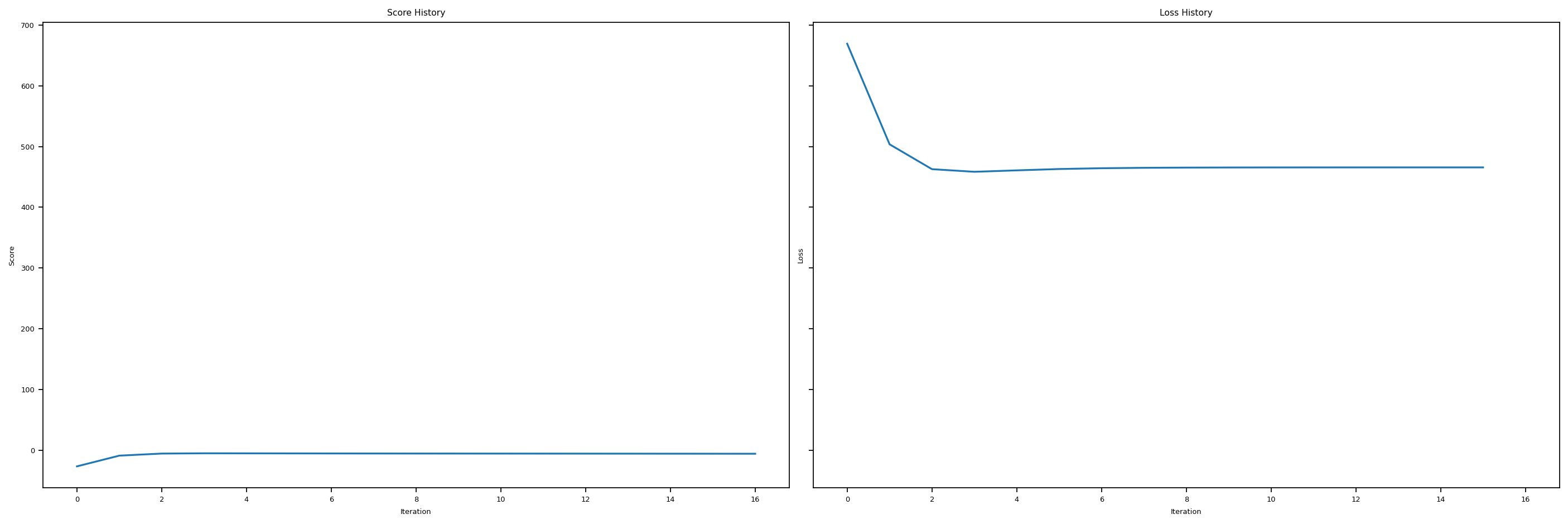

Validation Loss = 20.17Let’s plot the score history and loss history to get a better idea of what’s going on here. We see that we get pretty low scores, and our loss history doesn’t look very good. Hence, our OLS regression is not super good when the number of features gets to large.

LR5 = LinearRegression()

LR5.fit_gradient(X_train_, y_train, 0.0001, 1000)

print(f"Training score = {LR5.score(X_train_, y_train).round(4)}")

print(f"Validation score = {LR5.score(X_val_, y_val).round(4)}")

# plt.plot(LR2.score_history)

# labels = plt.gca().set(xlabel = "Iteration", ylabel = "Score")

# plot it

fig, axarr = plt.subplots(1, 2, sharex = True, sharey = True)

axarr[0].plot(LR5.score_history)

axarr[1].plot(LR5.loss_history)

labs = axarr[0].set(title = "Score History", xlabel = "Iteration", ylabel = "Score")

labs = axarr[1].set(title = "Loss History", xlabel = "Iteration", ylabel = "Loss")

plt.tight_layout()Training score = -5.9295

Validation score = -6.2086

In this last section, let us recall that LASSO uses a modified loss function of the following expression: \[ L(w) = \lVert X \cdot w -y \rVert ^2_2 + \sum_{j=1}^{p-1} \alpha \cdot | w_j |. \] And hopefully, LASSO will be a better option when number of features gets too big.

L2 = Lasso(alpha = 0.01)

n_train = 30

n_val = 30

p_features = 1

noise = 0.2

p_features = n_train - 1

X_train, y_train, X_val, y_val = LR_data(n_train, n_val, p_features, noise)

L2.fit(X_train, y_train)

L2.score(X_val, y_val)0.5877132844037414Hey, this score is not bad!

LR4 = LinearRegression()

LR4.lasso_score(n_train, n_val, noise)

LR4.lin_regress_score(n_train, n_val, noise)

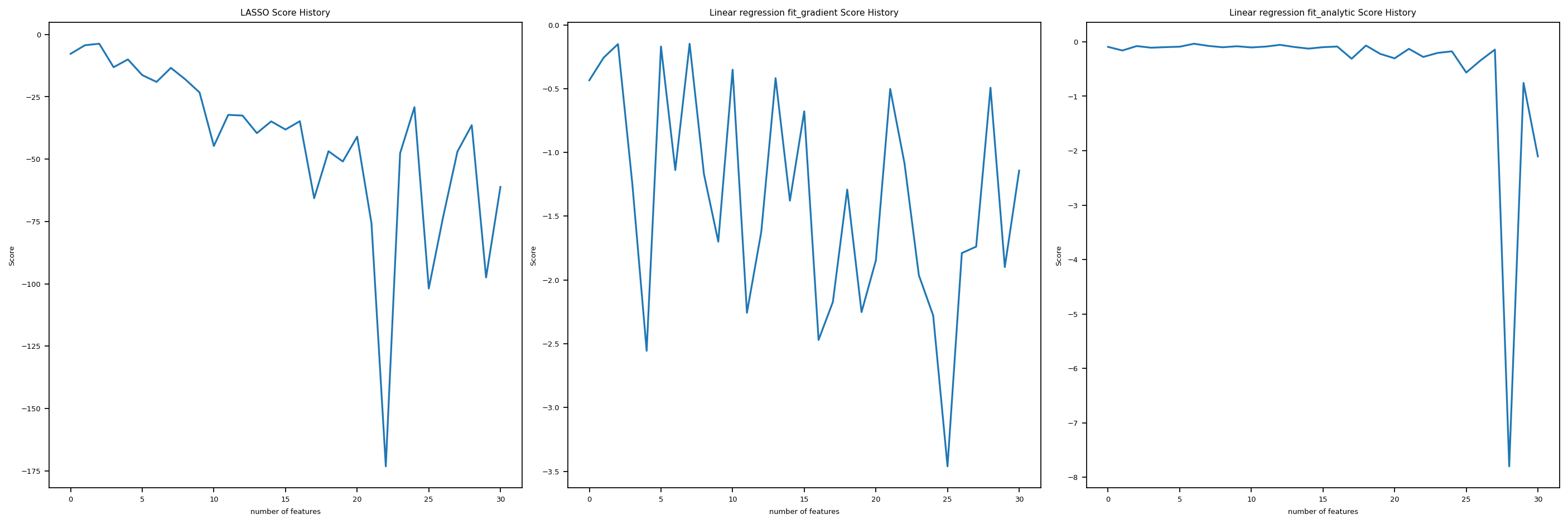

LR4.lin_regress_score_analytic(n_train, n_val, noise)Let’s use a custom function that we implemented in linear_regression.py to increase the number of features one by one, and for each number of feature, we generate a new sythetic data set and fit the \(3\) regressions we introduced so far. Then we plot the Score history for all three regressions against number of features, so y-axis is score, and x-axis is number of features. In this way, we could see clearly how fit_gradient, fit_analytic, and LASSO perform as the number of features increases to up to \(n\), which is the number of data points.

# from matplotlib.pyplot import figure

# figure(figsize=(8, 6), dpi = 156)

fig, axarr = plt.subplots(1, 3, sharex = False, sharey = False)

axarr[0].plot(LR4.lasso_score_history)

axarr[1].plot(LR4.fit_gradient_score_history)

axarr[2].plot(LR4.fit_analytic_score_history)

labs = axarr[0].set(title = "LASSO Score History", xlabel = "number of features", ylabel = "Score")

labs = axarr[1].set(title = "Linear regression fit_gradient Score History", xlabel = "number of features", ylabel = "Score")

labs = axarr[2].set(title = "Linear regression fit_analytic Score History", xlabel = "number of features", ylabel = "Score")

plt.tight_layout()

We see, it turns out that all three are not doing super well as the number of feature increases. The score goes up and down wildly, and especially for fit_analyitic, it seems that the score just fall off the cliff at one point and then bounced back somehow. Hence, as the number of features increases too much, we tend to have problems with the three regressions we introduced in this post.

The Python source files used in this post are reproduced below so that readers of the rendered site can inspect the implementation without needing access to the underlying repository.

linear_regression.pyimport typing

from typing import TypeVar

from sklearn.linear_model import LogisticRegression

from mlxtend.plotting import plot_decision_regions

from scipy.optimize import minimize

from sklearn.linear_model import Lasso

import random

import numpy as np

# functions from https://middlebury-csci-0451.github.io/CSCI-0451/lecture-notes/gradient-descent.html

class LinearRegression:

def __init__(self):

self.y = None

self.w = None # w_gradient

# self.w_analytic = None # w_analytic

self.new_loss = None

self.loss_history = []

self.score_history = []

self.L = Lasso(alpha = 0.001)

self.lasso_score_history = []

self.fit_gradient_score_history = []

self.fit_analytic_score_history = []

def y_hat(self, X, w):

return X@w

def loss_ell(self, y_hat, y):

return (y_hat - y)**2

def empirical_risk(self, X, y, loss, w):

y_hat = self.y_hat(X, w)

return loss(y_hat, y).mean()

def Big_L(self, X_, y) -> float:

return np.linalg.norm(self.y_hat(X_, self.w)-y, ord = 2)

def gradient(self, P, q):

return P@self.w - q

def fit_gradient(self, X_: np.array, y: np.array, alpha: float, max_epochs: int) -> None:

features = X_.shape[1]

self.w = np.random.rand(features,1)

self.score_history.append(self.score(X_,y))

# initialization

prev_loss = self.Big_L(X_ = X_, y = y) + 0.99

done = False

i = 0

P = X_.T@X_

q = X_.T@y

# print(f" this is self.gradient {self.gradient(P,q)}")

# while loop iteration

while (not done) and (i <= max_epochs):

self.w = self.w - 2 * alpha * self.gradient(P, q) # gradient step

self.new_loss = self.Big_L(X_ = X_, y = y) # compute loss

# check if loss hasn't changed and terminate if so

if np.isclose(self.new_loss, prev_loss, rtol=1e-05, atol=1e-08):

done = True

prev_loss = self.new_loss

# update before next loop

self.loss_history.append(self.new_loss)

self.score_history.append(self.score(X_,y))

i += 1

def fit_grad(self, X_: np.array, y: np.array, alpha = 0.00001, max_epochs = 50) -> None:

features = X_.shape[1]

self.w = np.random.randn(features,1)

# initialization

prev_loss = self.Big_L(X_ = X_, y = y) + 0.99

done = False

i = 0

P = X_.T@X_

q = X_.T@y

# while loop iteration

while (not done) and (i <= max_epochs):

self.w = self.w - 2 * alpha * self.gradient(P, q) # gradient step

self.new_loss = self.Big_L(X_ = X_, y = y) # compute loss

# check if loss hasn't changed and terminate if so

if np.isclose(self.new_loss, prev_loss, rtol=1e-05, atol=1e-08):

done = True

prev_loss = self.new_loss

i += 1

def fit_analytic(self, X_: np.array, y: np.array) -> None:

w_hat = np.linalg.inv(X_.T@X_)@X_.T@y

# self.w_analytic = w_hat

self.w = w_hat

def predict(self, X_) -> np.array:

return X_ @ self.w

def accuracy(self, X: np.array, y: np.array, w: np.array, ) -> float:

pass

def score(self, X_, y) -> float:

n_of_points = X_.shape[0]

y_hat = self.y_hat(X_, self.w)

y_bar = y.mean()

quotient = ((y_hat - y)**2).sum() / ((y_bar - y)**2).sum()

result = (1- quotient)/n_of_points

return result

def pad(self, X):

return np.append(X, np.ones((X.shape[0],1)), 1)

def data(self, n_train = 100, n_val = 100, p_features = 1, noise = .1, w = None):

if w is None:

w = np.random.rand(p_features + 1) + .2

# print(w)

X_train = np.random.rand(n_train, p_features)

y_train = self.pad(X_train)@w + noise*np.random.randn(n_train,1)

X_val = np.random.rand(n_val, p_features)

y_val = self.pad(X_val)@w + noise*np.random.randn(n_val,1)

return X_train, y_train, X_val, y_val

# n_train = 100

# n_val = 100

# p_features = 1

# noise = 0.2

def lasso_score(self, n_train: int, n_val: int, noise: float) -> None:

for p_features in range(1, n_train+2):

X_train, y_train, X_val, y_val = self.data(n_train, n_val, p_features, noise)

# X_train = self.pad(X_train)

self.L.fit(X_train, y_train)

self.lasso_score_history.append(self.L.score(X_val, y_val))

def lin_regress_score(self, n_train: int, n_val: int, noise: float) -> None:

for p_features in range(1, n_train+2):

X_train, y_train, X_val, y_val = self.data(n_train, n_val, p_features, noise)

# X_train = self.pad(X_train)

self.fit_grad(X_train, y_train)

self.fit_gradient_score_history.append(self.score(X_val, y_val))

def lin_regress_score_analytic(self, n_train: int, n_val: int, noise: float) -> None:

for p_features in range(1, n_train+2):

X_train, y_train, X_val, y_val = self.data(n_train, n_val, p_features, noise)

# X_train = self.pad(X_train)

self.fit_analytic(X_train, y_train)

self.fit_analytic_score_history.append(self.score(X_val, y_val))